The Albanese Government has released its second National Defence Strategy (NDS) along with a supporting Defence Integrated Investment Program (IIP). This follows the 2024 version. That was the first in a new approach to defence strategic policy planning which was intended to replace intermittent white papers with a series of NDS documents released on a regular two-year drum beat.

These kinds of documents tend to resemble Impressionist paintings: you can make out the broad outlines, but on closer inspection the details get blurry. And the further in you go, the muddier it becomes. The 2026 IIP is no exception.

Nevertheless, there’s enough information there to draw some high-level conclusions about the dollars but also enough that’s fuzzy enough to raise some questions. We’ll focus here on the top level budget line and the balance of investment between key cost categories (i.e., acquisition, operating and personnel costs) and between capability domains.

We won’t look in detail at the Government’s rather interesting claim that by adopting the NATO definition of defence spending, Australia’s defence spending increases by roughly 33% to 2.8% of GDP. That’s the topic for another essay but we can see signs of this new method of counting in the analysis below.

The top level

Like its predecessors, the 2026 NDS follows the practice begun in the 2016 White Paper of setting out a 10-year funding line. That is presented on page 85 of the 2026 NDS. This covers the Department of Defence, the Australian Signals Directorate, the Australian Submarine Agency and (starting very recently) the Australian Naval Nuclear Power Safety Regulator. We assume this line represents the Government’s appropriations for those agencies, but as we discuss below there may be some caveats around that assumption. We’ve compared the top level funding line in the 2026 NDS with previous strategic documents in Table 1.The 2026 NDS’s year on year funding line is reproduced in Table 3 below.

Table 1: Defence funding line in strategic documents

The numbers are certainly getting bigger each time round. At this rate we’ll hit a trillion over the decade by the time the 2028 NDS comes around, but it’s important not to confuse nominal increases with actual increases in funding. Departmental budgets generally go up as the population and economy grow and numbers increase due to inflation. So it’s not surprising that each successive document has a bigger funding line.

But there are actual increases in them as well. Next we’ll consider the actual increases, or as the media likes to term it, ‘new money’.

How much additional money is there?

The 2026 NDS states that ‘the Government is investing an additional $14 billion over the next four years and $53 billion over the next decade. This brings the combined additional investment across the 2024 National Defence Strategy and the 2026 National Defence Strategy to $30 billion over the next four years and $117 billion over the decade to 2035–36.’

In other words, the claims are that the new NDS has increased defence funding by $14 billion over the forward estimates and $53 billion over the decade compared to the 2024 NDS and that, together, the two Albanese government National Defence Strategies have increased funding by a combined $30 billion and $117 billion (more precisely, $29.8 billion and $117.4 billion) compared with…, compared with what exactly? What is the baseline being used? Let’s unpack both of these claims.

Coalition vs Labor funding

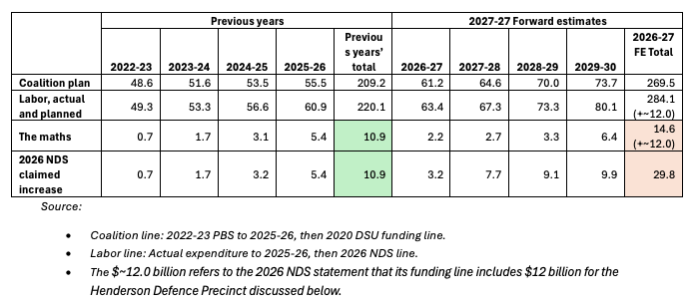

We’ll start with the second one. In a defence funding backgrounder circulated to the media, the current government is making its claim against the funding line the previous government left behind when they departed office shortly after delivering their 2022-23 budget. That budget gives planned numbers out to 2025-26, which overlaps with the Albanese government’s first four years in office.

The backgrounder claims that over those past four years, the current government has delivered $10.9 billion more in defence funding compared to the previous government’s plan. We’ve reviewed the numbers and that claim checks out (see Table 2 below).

That funding represents a 5.2% increase. Of course, one might wonder whether a 5.2% increase is commensurate with the current government’s repeated assessments of increasing strategic uncertainty, growing risk and general pessimism—America is planning a roughly 40% increase in the Pentagon budget in a single year, as a comparator for making change when times change. But the claim is verifiable and correct.

It’s when we look forward that the claim gets a little shakier. The only public source we have for the Coalition’s funding plan from 2026-27 is the 2020 Defence Strategic Update (DSU). The Coalition may well have changed their funding plan for those later years from what was in the Update, but there’s nothing on the public record to say what that might have been, so we’ll have to go with what’s in the Update for the year’s 2026-27 to 2029-30.

When we compare the 2020 DSU and the 2026 NDS funding lines over the forward estimates starting in 2026-27, the maths says the increase is $14.6 billion. That is significantly less that the Government’s claim of $29.8 billion—there’s a $15.2 billion gap. We’ll attempt to reconcile the two figures below.

We can’t validate the ‘total additional investment’ claim of $117 billion over the decade to 2035-36 because isn’t any public information on what the Coalition’s planned funding line was past 2029-30 out to that point. We could attempt to apply some metrics to extend the DSU’s funding line out another six years but that’s getting pretty hypothetical.

Table 2: Comparison of planned Coalition and Labour defence funding, 2022-23 – 2029-30

2024 vs 2026 NDS funding

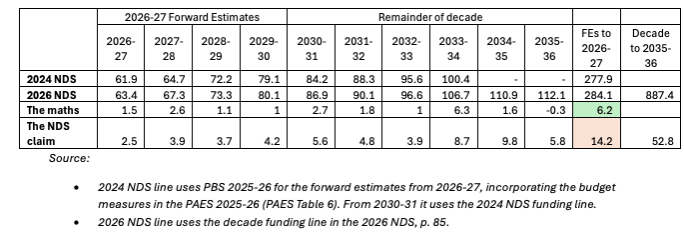

Let’s now look at the first claim, namely that the 2026 NDS delivers $14 billion additional funding over the 4 years in the forward estimates and $53 billion over the decade compared to its 2024 predecessor. Again, we have the baseline issue. We assume it is the funding line in the 2024 NDS, however in Table 3 below we have tweaked that line to include the adjustments in the Portfolio Budget Statements and Portfolio Additional Estimates Statements over the past two years.

Table 3: Comparison of 2024 NDS funding with 2026 NDS funding

Again, when we do the maths, we see that the actual increase of $6.2 billion over the forward estimates falls well short of the claim of $14.2 billion, a gap of $8 billion (incidentally, if we use the ‘pure’, unadjusted 2024 NDS funding line as the baseline for the comparison, the increase is even smaller at a rather underwhelming $1.1 billion over the forward estimates).

Again, we can’t assess the claim over the whole decade because there’s no public figures for the NDS 2024 funding line after 2033-34. But in the eight years out to 2033-34 where the two documents overlap, the claim is $37.3 billion in additional funding, but the maths says it’s only $18 billion, a gap of $19.3 billion. Based on that, we can probably assume that difference over the full decade would be well short of the claimed $52.8 billion.

Accounting for the gap

So what accounts for the shortfall between the claims and the numbers for both the Coalition-Labor comparison and the 2024 NDS-2026 NDS comparison? One likely reason is that the 2026 NDS includes has a footnote on page 86 stating that the total additional investment in defence capability includes ‘$12 billion investment in the Henderson Defence Precinct.’ The Government made that announcement in September 2025 so it’s not exactly new news.

But that statement presents a number of issues. First, we don’t know how the $12 billion is spread out, in particular how much is in the forward estimates and how much is in the rest of the decade. But if a big chunk of it is in the forward estimates, it would help reconcile the discrepancy between the claimed increases and the actual numbers in both of the comparisons above in the forward estimates. Given concept studies about the Precinct are still being conducted and thoughts about its financing are still being had, it’s difficult to see too many billions galloping out the door on actual precinct construction any time soon.

Second, in the September 2025 announcement, the Government said that the $12 billion was just the first instalment of a total of $25 billion ‘over the decade’—but there’s no mention of the other $13 billion in the NDS. It may also be being counted in the ‘additional funding’ without being mentioned. If it is, then that also would help reduce the discrepancy. Or it may have evaporated, or it may reappear in the next NDS.

Finally, the $12 billion/$25 billion likely isn’t part of the Defence portfolio’s funding. Construction of the surface ship and submarine shipyards at Osborne in South Australia was funded by equity injections from the Department of Finance. That’s appropriate because the Department of Finance is the owner of those facilities through the government-owned company Australian Naval Infrastructure. It’s not clear if the master plan for Henderson has been completed even while concept studies are on-going—it hasn’t been publicly released so we don’t know what parts of the complex will be government-owned. But if the Government takes a similar approach in Henderson, that $12 billion/$25 billion, or a large part of it, likely won’t not be Defence portfolio funding.

Historically in Australia we have not counted this type of Finance Department administered money as defence funding. It may be that the Government is counting it under as defence funding under the NATO methodology. However, in the NATO methodology for calculating defence funding, construction of shipyards doesn’t count towards defence spending, at least not towards the 3.5% of GDP goal of spending on ‘core defence requirements.’ However, the NATO spending target also includes a somewhat fuzzier additional 1.5% of GDP (for a total of 5%) that includes ‘strengthening the defence industrial base’ so the Henderson funding could probably fit in that category.

So we can already see how the Government’s appeal to the NATO methodology is beginning to muddy the waters around how we count defence funding. The $12 billion planned spend on Henderson doesn’t appear to be part of the 2026 NDS funding line in the document itself, but Government is nevertheless counting it as a defence funding increase.

Overall, if we consider that a big part of the $14 billion in claimed additional funding over the forward estimates is probably made up of a large chunk of the $12 billion in shipyard funding (that likely isn’t part of the Defence Department’s appropriation), it doesn’t appear to be the case that much of that $14 billion is programmed to acquire actual military capability in the near term. Or do anything that wasn’t already in the works under the 2024 NDS.

Alternative financing – other people want good returns for using their cash

The other element of ‘funding’ that may account for the discrepancy in our comparisons above is the 2026 NDS’s discussion of ‘alternative financing’. What is alternative financing? The NDS states The NDS states (paragraph 10.6) that:

‘the Government has identified around $5 billion over the forward estimates and $15 billion over the decade in projects for which Defence will prioritise developing alternative financing delivery options.’

It also states (paragraph 10.5) that alternative financing:

‘can include equity-based financing through Commonwealth bodies such as specialist direct investment vehicles and government business enterprises, as well as private financing.’

Is that alternative funding part of the ‘missing’ additional money discussed above? A second budget backgrounder released just before the 2026 NDS states that:

‘the Government is investing an additional $14 billion over the next four years and $53 billion over the next 10 years above the trajectory set out in 2024 NDS, through Defence funding, net proceeds from estate divestment and alternative financing where feasible and there is value for money.’

That seems to be a clear statement that the alternative financing is part of the additional funding. But to us, that seems a little dodgy: private financing shouldn’t be categorised as defence funding when it’s not part of the budget appropriation and isn’t the Government’s money. Conversely, if we are talking about government business enterprises acquiring or building assets using an equity injection from the Government, then it’s not alternative financing—it’s government funding.

It may be that this $5 billion / $15 billion is not part of the Defence portfolio appropriation (it’s not clear how the Auditor-General could sign off on Defence’s accounts if it were), but this is something else that the Government is counting as defence funding under the NATO definition. It’s an issue worth clarifying at Senate Estimates hearings.

There’s nothing new in getting the private sector to finance and build infrastructure that the public sector then leases back. Defence Minister Richard Marles admitted as much in his speech launching the NDS, citing an example where private equity built a facility near Bungendore in NSW that Defence pays the owner rent and service fees to use. What is new is the current government’s rhetorical zeal for such approaches, stating in February this year that ‘to turbo charge our home-grown defence industry, the Australian Government is seeking proposals from Australia’s private capital market for potential co-investments in local industry.’

Arguments about whether such approaches (termed Public-Private Partnerships, or Contractor-Owned, Contractor-Operated) present better value for money for taxpayer have gone around for years. Advocates say the private sector can build and operate facilities more efficiently that the public sectors. Critics say that superannuation funds and private investors generally expect a rate of return on their investment that exceeds the cost to the government of borrowing money to build it itself. That can make the economics of this type of finance compared with good old government debt look poor once the celebrations around announcements end. Moreover, private capital is unlikely to invest in R&D in new military technology without a guaranteed return—something that potentially undermines the competitiveness of defence tenders.

Where you stand on this is probably determined by where you stand on the broader question of whether the Government should retain or outsource the ownership and operation of functions where there appears to be a natural monopoly, like water and sewerage or electricity transmission or defence.

Either way, $5 billion over forward estimates and $15 billion over decade is only a tiny fraction of $887 billion (around 1.7%). It’s not going to transform the way the government funds defence or the way the portfolio does business. And there are some early indications that calculus doesn’t stack up for the big superannuation funds that the Government is hoping to tap, so even that 1.7% in ‘alternative financing’ may be a pipedream.

Defence funding as a percentage of GDP

The 2026 NDS states that under the NATO definition, Defence spending will rise to approximately 3.0% of GDP by 2033-34. It doesn’t provide a figure for any other year, but Marles stated in his speech that ‘today we are spending 2.8% of GDP on defence.’ Unfortunately, the Government has not provided any evidence to back that claim up, such as a break down of what it is counting towards that 2.8%, so we can’t validate it (we’ll examine it in a separate piece).

But even if the Government’s application of the NATO methodology is correct, it is rather underwhelming that the Government is only planning to increase defence spending by 0.2% over the next eight years. It’s also well short of NATO’s goal of 3.5% of GDP on ‘core defence requirements’ and the Trump administration’s expectation of the United States’ partners and allies.

In Table 4 below we’ve presented the ‘historical’ way of assessing defence spending as percentage of GDP which uses the government appropriation for the Defence portfolio. Of course we have to add in all the obligatory warnings that predicting GDP is a mug’s game. We’ve simply taken the predictions for the forward estimates in the latest budget documents and extended out by 5.3% nominal growth each year. If we have high inflation (as we are experiencing now), the economy will grow faster in nominal terms, and defence spending will consequently decrease as a percentage of GDP even if the government delivers the dollars.

Table 4: Planned defence spending as a percentage of GDP

The 2024 NDS aimed to increase defence spending to 2.33% of GDP by the end of its decade in 2033-34. The 2026 edition shows a modest increase on that of 2.47% in 2033-34. But that’s still four NDS’s away and many future ups and downs in GDP trajectories.

Reprioritisations

The Government has stated in a backgrounder that ‘it remains committed to making the necessary and as needed, tough, decisions to cancel, divest, delay or re-scope projects.’ Unfortunately we don’t know what that toughness resulted in.

When the Government released the 2024 NDS, Marles stated that there had been reprioritisation of ‘$22.5 billion over the next four years and $72.8 billion over the decade’ of capability. It also circulated backgrounders to the media with a list of the largest reprioritisations. This time round we have seen no information, either on the dollars or the capability involved in any reprioritisations. No doubt some are there, but by and large they are buried below the top level capability funding lines in the IIP.

Medium-range ground-based air defence and ballistic missile defence disappeared from the 2024 IIP, a truly perplexing decision in light of what had been occurring in Ukraine over the preceding two years and the 2024 NDS’s own admission that distance no longer protected Australia from long-range strike threats—the irrationality of that decision has been reinforced by the current conflict in the Middle East. The 2026 NDS partially reverses that, stating that there will be ‘new investment in a medium-range, ground-based air defence system to defeat advanced aircraft and missiles. This program will commence as a priority from 2026.’ That program is one part of a large $7.2-10 billion investment in active missile defence sometime over the next ten years.

The first imbalance: 42% acquisition spending

We’ll now consider three areas of potential imbalance in the 2026 NDS and IIP.

As all Douglas Adams fans know, 42 is the meaning of life. It also seems to be an obsession for Defence’s acquisition planners—and like most obsessions, it’s out of touch with reality.

Broadly speaking, we can divide the budget of any organisation into three main categories: its capital or investment budget, its operating budget, and its people costs. In Defence, the Big 3 are acquisition, operating—which is largely sustainment of its capabilities, and workforce.

The 2016 Defence White Paper set a goal of growing acquisition’s share of the budget from around 30% (it used the term ‘capital’) to reach 39% by the end of its decade in 2025-26. However, by the time the 2020 Defence Strategic Update was released, acquisition spending had actually declined as a share of the budget to 28.6%. Undeterred, Defence planners increased the target to 40% of budget by the end of the DSU’s decade.

This pattern repeated itself in the 2024 NDS. Acquisition spending should have reached 37% by 2024 under the DSU model, but Defence had only achieved 32%. Once again undeterred, Defence planners increased the goal to 42% of the total defence budget by the end of the 2024 NDS’s decade.

2025-26, the current budget year, is the final year of the 2016 White Paper’s decade and Defence has reached 34.1%. Over ten years Defence has managed to move the dial by 4% from its starting point in 2016, falling well short of the original goal of 39%. Nevertheless, Defence planners are nothing if not persistent and the 2026 NDS remains committed to reaching 42% by the end of the new decade.

This is not quibbling about numbers. To deliver the capabilities set out in its investment plans, Defence has to hit those acquisition spending goals. If you don’t spend the money, you don’t get the capability. Because Defence hasn’t been able to hit its acquisition spending targets since the 2016 white paper, it has underspent its target over the decade by a combined $24.2 billion, or 15%. That’s $24.2 billion in capability that hasn’t been delivered.

There are several reasons for this underperformance. There is an institutional one, namely Defence’s well-documented inability to deliver on schedule. But there is likely a fundamental structural one also. While there is no perfect balance between the Big 3, there do appear to be limits. Put simply, if you are acquiring more equipment, you also need to spend money to maintain and operate it as well as employ people to use it, so the relative percentages remain broadly in balance. That’s supported by the fact that the flip side of Defence underspending its acquisition target by $24.2 billion over the past decade is that it overspent its sustainment target by almost $20 billion.

It may be the case that in wartime when governments are acquiring large amounts of materiel that will almost immediately be destroyed that the balance can swing strongly in favour of acquisition. But the 2026 IIP is a peacetime plan based on acquiring things once and keeping them for the long term. We remain sceptical that Defence will achieve a 42% acquisition spend. That means the capabilities in the IIP will not be delivered on time.

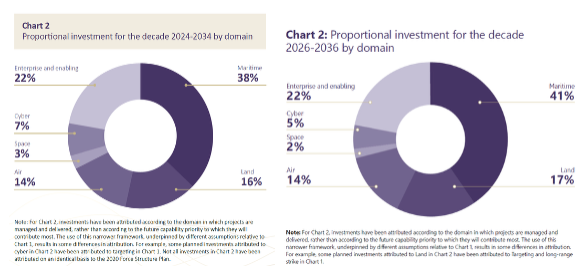

The second imbalance: 41% maritime spending

When the 2024 IIP was released, many observers were surprised by the percentage of the investment budget that was going into maritime capability. At 38% it was a larger share than air, land and cyber capabilities combined, leading to many analysts to argue that the balance of investment across domains was seriously skewed. That extremely large percentage was driven by planned spending on the AUKUS SSN program ($53-63 billion over the decade) and the Hunter-class frigates. Strategic Analysis Australia noted that that imbalance was likely to endure, potentially for decades as the big shipbuilding projects were joined by the General Purpose Frigates, all three continued to ramp up and entered full-rate production.

Despite that prediction, it is still somewhat jarring to see that the imbalance has become even more severe just two years on, in the 2026 IIP. Maritime capabilities now constitute 41% of the program and we can add space to air, land and cyber as areas that in combination are still outweighed by the single maritime category.

Figure1: Investment by domain in the 2024 and 2026 Integrated Investment Programs

The growth in maritime spending is driven primarily by two factors. The first is that the planned spend for the SSNs over the coming decade has risen to $71-96 billion. We wrote after the 2024 NDS that the AUKUS SSN program essentially costs as much as a fourth ADF service. That’s been confirmed in 2026 NDS with that one program alone at 16.7%-22.6% of the total IIP, more than either Air (14%) or Land (17%).

The increase from 2024 to 2026 is not (necessarily) driven by the cost of the program going up. Rather, two (relatively) ‘small’ years of spending have passed (2024-25 at $2.7 billion and 2025-26 at $3.9 billion), while the two new years entering the back end of the decade are probably each budgeted at over $10 billion each as Australia will not only be buying Virginias but ramping up spending in the UK on SSN-AUKUS and on Aussie construction in Adelaide. So $6.6 billion passing into history and $25 billion coming in accounts for the increase.

The second factor is that the 2024 IIP’s decade spend for the General Purpose Frigates was $7-10 billion. That’s gone to $15-20 billion. That increase is a little harder to explain simply through annual cash flow increasing over the years (even though the program has spent very little in 20204-25 and 2025-26) and it may well be that the estimate has actually gone up as Defence learned more about the program through the tender process and contract negotiations over the past two years. We should note that $15-20 likely isn’t the total cost of the program as some of the planned 11 ships will still be under construction well past 2035-36. Maybe those ‘minimal changes’ have turned out to be not the minor and not that cheap…

Overall, the Big 3 shipbuilding programs of SSNs, Hunter and GPF have gone from $82-105 billion to $113-148 billion. If we pick a mid-point of $130 billion, those three programs comprise 30.6% of the IIP’s total budget of $425 billion. That will almost certainly increase in the next IIP as both the SSN and GPF programs spending will need to ramp up significantly in the next few years. So 41% may not actually be the limit of the imbalance. It’s beyond the scope of this essay to consider what impact that will have on the rest of the force structure.

The third imbalance

We noted above that the public IIP resembles an impressionist painting with few details. There is no doubt a lot of detail in the classified version of the IIP, but we don’t have access to that. This allows the Government to pull numbers out of the classified IIP at will and repackage, mix and match them to serve any purpose it desires.

We can take as an example, small autonomous systems, the sorts of things that have transformed warfare in Ukraine and are allowing Iran to close the Straits of Hormuz. There is no specific line for ‘smaller uncrewed systems’ in the IIP, but the Government released a backgrounder stating that ‘investment in smaller uncrewed systems alone will total $2.2-$3.1 billion across all domains.’

But if this unverifiable number was meant to impress, it only achieves the opposite. That figure is around 1/30 of the planned budget for one single capability, the SSNs, at $71-96 billion. Iranian’s smaller uncrewed systems have closed the Strait of Hormuz. The US Navy’s 48 SSNs have done nothing to open it.

US defence analyst Robbin Laird has written, after years of analysing the emergence of autonomous weapons that, ‘Western militaries have spent decades optimizing for peak performance per hull, per aircraft, per submarine. The drone wars have demonstrated that in a protracted, high-intensity conflict, that equation breaks down. What matters is not the single most capable platform but the ability to generate and sustain enough force across enough vectors to deny the adversary decisive advantage…. The drone wars taught us that affordability, manufacturability, and operational simplicity at scale can generate strategic effects that exquisite complexity cannot.’

The Government and Department of Defence have not yet internalised this lesson, let alone acted upon it. Perhaps more than any other number, the gulf between the spending in the NDS on SSNs and small autonomous systems reveals the fundamental imbalance in Defence’s investment plans and its divorce from reality.

Further analysis

In the near future we’ll look at the issue of the NATO definition as well as put out some analysis of the forthcoming 2026-27 defence budget. Hopefully the budget papers will shed some light on the issues raised here around what the actual increase to the Defence portfolio budget is. If it doesn’t and we are still left wondering what the actual Defence portfolio money is and what is other spending that might fall under a broader NATO definition, then Senate Estimates hearings should spend some time getting Defence to clarify issues.